Sherrilynn Palladino lives in a modest three-bedroom home with an affordable mortgage about a mile and a half from the ocean in Grover Beach, Calif. She’s never missed a mortgage payment during the 10 years she’s lived in the neighborhood. In fact, she says, she’s never late on any bills. At 60, she’d like to retire, downsize and escape spiraling property taxes in the suburb about half-way between Los Angeles and San Francisco.

But she can’t. The house next door is empty. It’s been vacant and in various states of disrepair for three years.

Palladino is a quiet victim of the housing market crash. Call her collateral damage.

“I’m stuck,” she said. “I can’t sell my house for what I paid for it with an empty eyesore next door. I can’t afford upkeep, maintenance, and property taxes. And I can’t retire until I downsize … I don’t know what to do. It’s all just a mess and I feel like it’s out of my control.”

Palladino is one of an estimated 14 million homeowners in America who are now under water — they owe more on their mortgage than the value of their homes. She has the misfortune of living in California, where one in three mortgage holders are under water. Things are even worse in other states: In Florida and Arizona, half of mortgaged homes are under water; In Nevada, the number is 70 percent.

While consumers facing foreclosure and banks facing bankruptcy dominate the economic headlines, millions of other Americans are suffering effects of the housing market collapse that, while subtler, are very real. Homeowners who are under water often can’t move to take advantage of new job opportunities, they can’t refinance and take advantage of low mortgage rates, and they generally feel rotten about their prospects.

Palladino, who is single, would sell her home if she could, move into a cheaper condo and trim her annual property tax bill of $4,700. But the house next door means that’s not in the cards.

“I didn’t buy more house than I could afford. I did everything I’m supposed to,” she said. “The mortgage is nothing. But it’s the taxes that worry me.”

What frustrates Palladino is that as far as she can tell, she’s done everything right. Ten years ago, she owned a condo in San Francisco and sensed that the market had become overheated, so she sold and moved to a more modest neighborhood three hours south.

“I had watched the peak and the Internet bubble break and decided to get out of that,” she said. “I made a killing selling that condo.”

She wanted to live at the beach, but instead took her hefty down payment and chose a modest single-story home that was a long walk away from the water.

“I still get the sea air. I can still smell it,” she said.

Following traditional financial advice, she bought as much home as she could afford without stretching too far — a three-bedroom, two-bath home with a fireplace for $419,000. Even with a modest return, she figured she’d be able retire in five to 10 years.

Now, she stares at the overgrown weeds covering the yard of the empty house next door and wonders if she will ever be able to retire — or if property taxes will slowly drain her life savings while she waits for a housing market rebound that may never come.”Every year I wait for a chance to put my house on the market but no luck as that eyesore continues to exist,” she said.

Things didn’t always look so bleak. At one point, they seemed positively magical. In April 2005, the house next door was sold to a family for $589,000. Palladino counted her lucky stars.

“I should have jumped, but I wasn’t ready,” she said. “I remember thinking, ‘Gosh, I can sell for a lot of money and use that for retirement, like you’re supposed to.’ ”

But three years ago, the house next door went back on the market — the couple that bought it was filing for divorce. That started the roller coast that Palladino is still on today. She watched the listing price fall, and fall, and fall, for nearly a year. At some point, the family moved out, and two years ago, the home was pulled from the market.

“That’s when it went downhill. Then the weeds started to grow,” she said. “I knew it was in foreclosure. At one point the weeds were five feet tall. Here I am trying to keep my place up and keep it looking nice, and what’s the point?”

For another year, the house sat vacant. Finally, this summer, a company came and painted the inside of the house. Even with that, the home remained empty through fall.

Then, at the end of September, it was listed for sale at $381,900 — almost $40,000 less than Palladino paid for her nearly identical home next door in 2002.

“No one knows they fixed up the inside from the outside,” she said. “I watch cars come down the street to take a look. They see the outside and drive right back out.”

That wasn’t the end of the roller coaster. The listing was removed in October, according to Zillow.com, suggesting a possible pending sale. But something went wrong, and the home was relisted for the same price on Oct. 17.

Why foreclosed homes take so long to sell

Banks aren’t in the business of buying and selling homes, yet with an estimated 6 million foreclosures during the last two years, mortgage issuers have turned into giant real estate outlet malls. All the big banks have real estate Web sites that seem like they belong at Zillow.com or MSN Real Estate.

Because banks, by definition, would rather hold mortgage paper than porches, you’d think they would rush foreclosure sales through the pipeline in an effort to dump properties and turn them into cash. That’s the main defense of the recent robo-signing controversy: Banks have claimed that they need to be as efficient as possible with foreclosures so the market can absorb the bad news and eventually cleanse all the distressed properties. Prolonging the process hurts everyone, they said.

But that’s not the whole truth.

Banks must also weigh the potential valuation disaster if they were to release all the foreclosed properties they own (known as REOs, or real estate owned) to the market simultaneously. So many empty homes would drive prices down drastically. That leaves banks in the position of throttling back their sales, trying to strike a balance between liquidating unwanted assets as soon as possible and widespread sales that devalue their own holdings.

That balance point is killing people like Palladino, who simply wants to move on with her life.

“I’m not getting any younger,” she said. “I have a number of health issues too, like arthritis. But for now I’ve got to keep working.”

Rick Koester, the sales agent for the empty house next door, said he now works exclusively on bank-owned home sales.

“I used to sell high-end homes, but this is all there is right now,” he said.

He wouldn’t discuss details of the home next door, citing ongoing sales negotiations, but said there are numerous reasons banks might hold onto foreclosed homes for what can seem like an eternity.

“There are a number of reasons banks do what they do. They don’t want to flood the market,” he said. “Iit’s usually a nine-month process when they start foreclosure to when the home sells.”

Accounting rules offer another possible explanation. In trying to explain why only 30 percent for foreclosed homes have reappeared on the open market in California, Sean O’Toole, CEO of research firm DataQuick, told the San Francisco Chronicle that banks are intentionally holding properties so they can exaggerate the value of those assets. In some cases, lost value doesn’t have to be acknowledged until foreclosed sales close in their accounting disclosures.

“With banks in the stress they’re in, I don’t think they’re anxious to show losses in assets on their balance sheets,” he told the paper.

Bank owned homes that are in limbo are called “Shadow Inventory” in the real estate industry. It’s unclear how many bank-owned homes are sitting empty, but not yet for sale, around the country, because banks don’t necessarily have to report them on their balance sheets. But attempts to quantify this Shadow Inventory have led to alarming conclusions. Earlier this month, Fitch Ratings said there are an estimated 7 million homes in this shadow inventory pipeline – and that it would take more than three years to sell all those bank-owned homes, Fitch said. As these trickle out onto the market, any fledgling recovery in home prices will be threatened, the ratings agency warned.

Palladino said she’s read that news, and sees it in real life every day. Empty, bank-owned homes dot her neighborhood, and she worries that even if the house next door sells, her home value will be depressed for years by the others.

“I don’t have a chance with all these other houses. I keep reading the recession is over. Oh really?” she said.

Even in the past week, Palladino’s sense of being jerked around by the housing market hit both new lows, and new highs. Koester said on Friday that the home next door has just been pulled from the market because of a pending sale. It hasn’t closed yet, and prior possible sales had fallen apart at the last moment, so he wouldn’t talk about it. But the news would provide a ray of hope for Palladino.

But on the other side of the Ledger, on Friday she was laid off from her job as an administrative assistant. She has savings to ease the blow, so she’s hard at work looking for a new job already.

“I cannot believe that people walk away from their responsibilities, like house payments. Never, never would I do such a thing,” she said.

Nov 10

22

Robotic signing validity disputed

NEW YORK — Bryan Bly is a pen-wielding “robo-signer” at Nationwide Title Clearing Inc., inking his name on an average 5,000 mortgage documents a day for companies such as Citigroup and JPMorgan Chase.

Those are just the ones that cross his desk.

Nationwide Title employs a computer system that automatically inserts a copy of Bly’s signature on thousands of digital files that he never sees. The system even affixes an electronic notary seal.

“The problem with the way these documents are created isn’t because a computer is used,” said Gloria Einstein, a legal aid attorney in Green Cove Springs, Fla., who deposed Bly in a case in a which her client faces foreclosure by a unit of Deutsche Bank. “It’s because an enterprise has decided to use a computer to create a system where nobody is responsible for the information and the decisions.”

The rush to securitize more than $4 trillion of mortgages as home sales peaked in 2005 and 2006 inundated loan servicers and contractors such as Palm Harbor, Fla.-based Nationwide Title that help them handle paperwork. Lawsuits fighting some of the more than 4 million foreclosures since then have exposed sloppy recordkeeping and raised questions about the validity of documents used to seize properties.

Bly is just one of more than a dozen robo-signers deposed in the past two years by lawyers for borrowers seeking to block foreclosures. Spurred by descriptions in depositions of employees signing thousands of affidavits a week without checking their accuracy as legally required, the attorneys general in all 50 states last month opened an investigation into whether banks and loan servicers used faulty documents or improper practices to foreclose.

Nationwide Title, which has about 175 employees, provides document imaging, tracking, retrieval, recording and processing on bulk loan transfers for lenders, servicers and investors. It’s the largest third-party processor of mortgage assignments, handling more than 350,000 last year, Senior Vice President Jeremy Pomerantz said in a telephone interview. The company prepares lien releases, too, which show that a mortgage has been paid off by the borrower.

Assignments, which usually are recorded with county land record departments, list the buyer and seller of a loan as it’s sold or packaged with other loans into a mortgage-backed security. Lawyers for homeowners are challenging the legitimacy of the documents, which are relied on by lenders to show they have the right to foreclose.

(While closely held Nationwide Title in the past offered a package of foreclosure-specific services, it had just one client, Pomerantz said. The company doesn’t handle foreclosure affidavits — submitted by banks to assert ownership of a loan when they’ve lost the promissory note or to show that borrowers are in default — and often, it doesn’t know when clients are requesting documents for defaulted loans, he said.)

Nationwide Title’s proprietary system isn’t entirely automated, said Erika Lance, senior vice president of administration. Employees receive requests from clients for lien releases and mortgage assignments, which often are sent in batches of as many as 30,000. They review the information and images of loan documents sent along with the request, and the information is keyed into the computer system.

The computer system fills in the electronic assignments in the format and wording each county requires, and places a signature and notary seal from a list of employees approved by each bank. Bly and other signers are given a title at the bank requesting the documents, such as “vice president” or “assistant secretary,” depending on what the individual counties require, Lance said.

Nationwide Title files documents with scanned signatures in the 10 percent of counties in the United States that accept electronic mortgage assignments, including those for cities such as Chicago, Miami and Seattle, according to Lance. She said producing electronic signatures in bulk is common in the industry.

“The laws are catching up to what is occurring with documentation,” she said. “Electronic recording is an accepted method of document recording.”

While the law allows for electronic signatures and seals on assignments and lien releases, the signer must physically appear before the notary, and the notary must affirm the signer’s identity, that the signer is aware of what the document is, and that the signer is willingly executing it, said Michael Robinson, executive director of the National Notary Association based in Chatsworth, California.

“The guiding principles behind it are the same as the guiding principles around paper notarizations,” he said.

Mark Ladd, a land-records technology consultant in Racine, Wis., said the systems he’s seen require that the signer acknowledge that he’s read the document and that the notary is physically present.

“The law requires that somebody review these documents themselves,” Ladd said. “The person who signs the document makes a statement that they read it.”

Nationwide Title’s Pomerantz declined to say whether the company’s system requires signers to affirm they have read the document. He said document inspectors, a job sometimes performed by signers and notaries, review signatures and seals on a computer monitor. The notaries know the identities of the signers because they work in the same office, he said.

“The signature is required to authorize it,” Pomerantz said. “The signature is not testifying in any way that they prepared that or personally validated the information. They rely on their staff to validate.”

Missing or incomplete paperwork has forced lenders to routinely recreate documents to show courts they have standing to seize properties, said Jim Miller, the executive who oversaw foreclosure-processing operations at JPMorgan Chase from 2005 to November 2008.

About a third of foreclosure files his teams handled were missing mortgage assignments. Servicers would often write new assignments when judges requested proof that the party seeking to repossess a property had the right to do so, he said.

“What used to happen before the robo-signer issues is that you’d find out while in the foreclosure process that assignments needed to be done, and you had time to clean it up before the actual foreclosure solidified,” Miller said in a telephone interview.

At JPMorgan Chase, where Miller was managing director of the default group, the company began fixing documentation prior to foreclosure more than two years ago in response to court rulings requiring lenders to show evidence of owning the loan before taking legal action, he said.

Miller is now an independent consultant for the mortgage- servicing industry based in Dallas. Thomas Kelly, a spokesman for New York-based JPMorgan Chase, declined to comment.

The issue for courts to decide is whether banks are seizing homes that they never legally acquired, visiting Harvard Law professor Katherine Porter told a Congressional Oversight Panel on Oct. 27.

The legal debate centers on whether assignments can be created to show transfers between banks that happened years earlier, Porter said.

“The largest and most complex harm that may exist with the loans in default or foreclosure today is that the paperwork for the loans was not transferred correctly,” Porter said. “I emphasize that what constitutes a correct transfer is a gray area; we need more direction from courts and legislatures on this subject.”

Paper documents were turned into electronic files so that they could be moved around quickly, and shortcuts were taken to accommodate multiple transactions, said Alan White, a law professor at Valparaiso University in Indiana. Promissory notes were endorsed in blank so that whichever company held it could claim possession. And mortgages were sometimes assigned in blank.

The foreclosure crisis opened up the process to scrutiny, as banks claimed to have lost thousands of promissory notes and were instead showing judges copies, White said.

Nationwide Title’s Lance said she has long recommended to corporate clients that they keep their files clean and produce assignments as transfers happen. Many of the assignments the company produces are for bulk sales from one bank to another, she said.

“NTC has been put in the middle of this storm,” she said.

Bly, 52, said he trusts the employees that have verified the assignments his signature is appearing on — even though he doesn’t know what those processes are and never sees the document.

“If they check it, why do they need you, sir?” Einstein, the attorney, asked Bly in his July deposition.

“As a signer,” he replied.

First, find out who is your loan holder. Don’t worry if you don’t know. Most people don’t have this information if there has never been a need for it before. Call Chase and a customer service representative will be happy to help you. If you are lucky enough to have a loan insured by Freddie Mac or Fannie Mae, then you will qualify for a goverment program designed to help you. This program will allow you to make payments that are no more than 31% of your monthly income.

How do you know if you meet the requirements for this plan? You must both own and live in the home and not owe more than$729,750. Furthermore, the loan should not predate January 1, 2009. If you already pay less than 31% of your total monthly income, you won’t qualify. This plan allows you to modify your loan only once. Contact your HUD office for more information if you think you may qualify.

While loans through Freddie Mac and Fannie Mae qualify for goverment funding, Chase is still able to assist you even if your loan is through a different lender. Though it won’t be as good of a deal (since there is no $75 billion bailout being applied to these programs), it’s still a lot better than foreclosure. To qualify for assistance through Chase, you must live in the house in question and it must be your first mortgage. You must not have previously refianced or modified a loan. Since there is no governmental assistance, you will need to be able to pay between 31% and 40% of your total monthly income. If you believe that you qualify you must submit a letter documenting the reason you are having difficulty making your payments, along with pay stubs, tax returns and other relevant financial documents.

By Ken McCall and Tim Tresslar

Staff Writers Updated 8:46 PM Saturday, November 20, 2010

Foreclosures dropped in Montgomery County last month after a flurry of allegations and lawsuits about shoddy filing practices caused four major lenders to suspend new filings.

But a Dayton Daily News examination shows the pace of foreclosures is gathering steam again in a region that is among the most hard-hit in Ohio.

More than 4,000 foreclosures have been filed in Montgomery County in 2010, while 1,200 were filed in Warren County and 703 in Greene. About half that number were filed in the three counties a decade ago.

The filings slowed last month after allegations erupted over faulty — critics say fraudulent — affidavits in foreclosure cases involving JP Morgan Chase, PNC Bank, GMAC and Bank of America. Ohio Attorney General Richard Cordray, who filed a lawsuit against GMAC over the affidavit practices, says lenders used “robosigners” to falsely swear to having reviewed documents in thousands of cases. One such signer for GMAC, Jeffrey Stephan, has admitted under oath to having signed 10,000 affidavits in one month.

The Daily News examined two of the affidavits signed by Stephen in Montgomery County, one for a house on Watervliet Avenue in Dayton and one in Englewood. In both cases he swore that he had “personal knowledge” of the documents in the foreclosure action.

“We think it’s fraud,” Cordray said of the robosignings.

Thomas Morano, head of GMAC’s mortgage operations, admitted to Congress last week that his company’s process for preparing foreclosure affidavits was “flawed.” During the same hearing, Stephanie Mudick of JP Morgan Chase said some employees may have mishandled aspects of the affidavit process, though she said the mortgage documents correctly listed the amount of money owed.

Montgomery County Common Pleas Court Presiding Judge Barbara Gorman said her staff is reviewing cases to determine the scope of the problem here.

When there are allegations of fraudulent documents filed with the court, she said, “We take that very seriously.”

Contact this reporter at (937) 225-2393 or kmccall@DaytonDailyNews.com.

One of the most heart-rending recurrences featured in the congressional hearing this past week about home mortgage foreclosure problems is the so-called “dual track” problem—when a family is negotiating a modification of its mortgage loan and suddenly the mortgage servicing company handling the monthly mortgage payments takes the home away before the modification takes effect. The hearing highlighted how mortgage servicers have two separate operations, with one office talking to customers about mods and another one keeping the foreclosure process moving at the same time.

The dual-track problem symbolizes why our foreclosure mess is so fundamentally unfair to too many families. Mortgage servicing companies (and the lenders and investors they work for to collect monthly mortgage payments) collect the documents needed to consider modifying the mortgages of many responsible but overburdened families, but then swoop in nonetheless to take the home away. Senator Jeff Merkley (D-OR) summed it up this way: “Can’t we just change this policy and suspend the foreclosure proceedings when a modification is underway, not keep it going forward and create this enormous confusion and stress for America’s families?”

Well, the Obama administration has taken significant steps to do just that, though more enforcement authority over mortgage servicing companies and their modifications are needed. The Obama administration’s much-maligned Home Affordable Modification Program, or HAMP, included Supplemental Directive 10-02, which was issued in March of this year and incorporated into the HAMP Handbook. This directive, which all the servicers that participate in HAMP (including all the major banks) have agreed by written contract to abide by, contains an entire set of consumer protections. Notably, servicers:

Can’t refer any loan to foreclosure until a borrower has been evaluated and determined to be ineligible for HAMP or reasonable solicitation efforts have failed

Must halt existing foreclosure actions when a homeowner begins a three-month trial modification

Cannot begin a foreclosure sale for 30 days after a written notice is given to the family that they have been turned down for a mortgage modification

Must still consider a request for a modification even as the time for a foreclosure sale nears, specifically until seven days before a foreclosure sale

These rules don’t apply in some circumstances, such as when the family has failed to make their monthly mortgage payments on a HAMP-modified loan. But the overarching principle at the heart of the HAMP directive is that foreclosures should not happen until homeowners get a fair shot at modifying their mortgage.

These rules are good for responsible homeowners because the rules are supposed to deal with the dual-track problem and protect families from unwarranted foreclosures until the modification process determines whether the homeowners can in fact pay monthly mortgages on a modified home loan. So why aren’t these rules a complete solution to the dual-track problem?

A big reason is that HAMP was created as part of the 2008 Troubled Asset Relief Program. TARP does not provide any statutory penalties or enforcement provisions for violations of HAMP. The lack of statutory authority limits Treasury’s enforcement powers even though servicers have signed contracts agreeing to follow HAMP rules and Treasury has created a compliance office for the program. Without enforcement power, too many servicers do not follow the rules they have agreed to.

Then there’s a trickier problem. HAMP consumer protection rules apply only to HAMP modifications, which meet eligibility requirements such as owner-occupied homes, moderate loan size, and loans made before 2009. HAMP rules don’t apply to other home loans, such as those over the HAMP dollar limit or those subject to contractual provisions imposed by some investors in the mortgage-backed securities in which so many home loans were packaged and sold. Probably more importantly, they don’t apply to non-HAMP mortgage modifications that servicers offer, such as the increasingly common practice where lenders offer their own terms for modifications and then don’t seek payment from the federal funds for HAMP.

Going forward, there are several steps that are administratively manageable for servicers and may be helpful to improve compliance by servicers with the HAMP requirements and address the dual track problem more generally.

First, violations of HAMP requirements should be reported to the HAMP program. Although far from perfect, there is a case escalation process designed to address problem cases under HAMP. The Treasury could usefully explain in greater detail what steps it is taking to ensure compliance with the HAMP requirements about the dual-track problem. And bank regulators could explore supervisory actions against mortgage service companies owned by banks that promise to follow HAMP rules but do not do so, or perhaps build these protections into banking regulations.

Second, the major banks should announce that they will halt the foreclosure process for the many loans on their own books, a step Bank of America at the recent congressional hearing says it is considering. The administration and Congress can keep a spotlight on this issue so that these common-sense measures are part of whatever reforms emerge in response to the robo-signing and other problems in the servicing sector.

Third, the Federal Housing Finance Agency should enforce HAMP consumer protection rules for the many loans serviced for Fannie and Freddie, the two mortgage finance giants now in federal conservatorship. There does not appear to be any public statement to date by FHFA that it expects the rules to be applied for those loans.

Fourth, the state attorneys general who are currently investigating robo-signing and other foreclosure-related problems should include stricter enforcement provisions in any settlements or consent decrees. A common feature of consent decrees is to have specific procedures to detect and enforce against continuing violations, and those procedures can apply to violations of HAMP rules.

Finally, Congress should consider whether to build protections against the dual-track problem into legislation. After all, the major banks have already agreed in writing to the federal government that they will follow these homeowner protections. Putting the agreements into a more enforceable form, for a wider range of loans, would be a useful step in making sure that these dual-track problems are reduced even further.

Peter Swire is a Senior Fellow at the Center for American Progress and the C. William O’Neill Professor of Law at the Ohio State University. Until this August, he served as special assistant to the president for economic policy, working extensively on housing and foreclosure issues.

By Ariana Eunjung Cha and Brady Dennis

Washington Post Staff Writers

Thursday, November 18, 2010; 11:10 PM

The financial services industry has launched an aggressive campaign on Capitol Hill to bolster the legality of the way companies have turned mortgages into securities and traded them across the globe in recent years. The companies have opened wide their wallets for lobbying and are flying top executives to Washington for one-on-one meetings with lawmakers. They are holding briefings for key staffers, including an event last week that drew more than 60 aides. And they are blanketing Congress with white papers, memos and other documents that lay out their arguments.

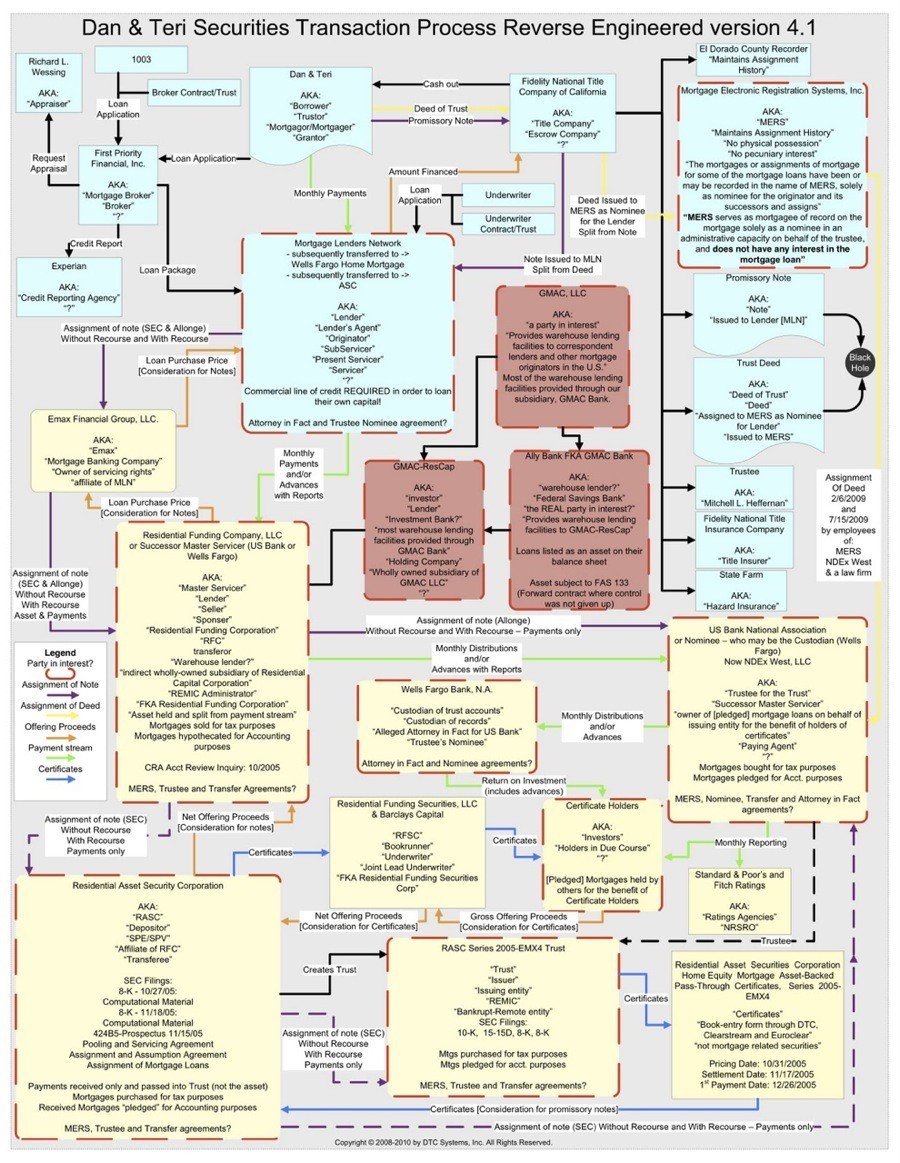

The focal point of their efforts is Mortgage Electronic Registration Systems, or MERS, the controversial, privately run electronic database that is used by practically every lending institution and investment company to track the transfer of the ownership of mortgages as they are packaged into securities and traded at lightning speed around the globe.

But MERS does more than just track the trading of loans. In the vast majority of mortgage documents at local courts and offices across the country, it is listed as the holder of the loans. That allows the financial industry to trade mortgages as much as it wishes without spending the time and money to refile the paperwork.

The industry is seeking legislation that would effectively affirm MERS’s legality and block any bill that would call into question what MERS does. MERS has spent more than $1 million in lobbying since fall 2008, when lower courts around the country began to rule against it. But MERS had kept its name under the radar until the recent uproar over foreclosures revealed broad problems in mortgage paperwork.

If successful on Capitol Hill, the industry could in one quick swoop make all lawsuits related to MERS across the country moot and remove one of the key uncertainties dangling over the mortgage industry. On the flip side, lawmakers could create a new federal registry, effectively killing MERS’s business and forcing the industry to submit to greater oversight.

In recent years, MERS has become the target of numerous legal challenges from homeowners in foreclosure who allege that mortgage transfers made through the system are invalid because they bypass local recording laws. MERS, the lawsuits contend, does not have standing to foreclose because it is only a database and not the actual holder of the mortgage.

The liabilities could be astronomical for MERS. One lawsuit in California alone is seeking recording fees that could cost the company from $60 billion to $120 billion. But the consequences for the financial industry are even greater, as challenges to the validity of transfers done by MERS call into question the entire process of how loans were securitized and could render the 66 million mortgages in its system foreclosure-proof. In the wake of such controversies, lobbyists for Reston-based Merscorp, which runs MERS, have been floating the idea of legislation that would establish the firm as the national registry to track the transfer of mortgages.

The MERS database “is a powerful tool that can be harnessed by the Congress and the industry to improve the mortgage finance system,” R.K. Arnold, Merscorp chief executive, told members of the Senate banking committee this week.

Tom Deutsch, deputy executive director of the American Securitization Forum, an industry group that defended the validity of MERS in a recent paper being circulated on Capitol Hill, said establishing a centralized tracking system would resolve much of the confusion resulting from the patchwork of local laws governing mortgages and their transfer.

“There’s a lot of validity in the idea of a national mortgage registry that is complete and unambiguous about legal title to loans across all 50 states,” he said in an interview. In its paper, the forum argued that although there have been “several minority decisions” in the courts that have taken issue with MERS, “not one of these decisions has challenged MERS’ ability to act as a central system to track changes in the ownership.” Consumer advocates say such legislation would retroactively bless all mortgage transfers made through MERS – and eliminate one of the strongest legal arguments that homeowners in foreclosure are using to challenge their cases. There’s also concern among state officials that such a bill might permanently remove some of their power over property law and place it within federal jurisdiction.

Some of the advocates are referring to the idea as the “great MERS whitewash bill.”

“Fixing MERS on a federal level to give them a free pass from complying with what we have known as the law for many years because the banks screwed up is really a bad precedent,” said Ira Rheingold, executive director of the National Association of Consumer Advocates.

The industry is also facing skepticism from Democrats such as Rep. Marcy Kaptur (Ohio), who is known for her strong opposition to the federal government’s bailout of Wall Street.

Kaptur plans to introduce legislation that would prohibit government-controlled mortgage financiers Fannie Mae and Freddie Mac from buying new mortgages that are in the MERS system. “It was invented by the most powerful financial players in the country while regulators were asleep at the wheel,” Kaptur said in an interview.

Kaptur is not opposed to a national system for tracking mortgages. She’s asking the Department of Housing and Urban Development to study how a federal land title system could operate in a way that would protect states’ rights. But she said there needs to be more transparency and regulatory oversight over such a system.

John Taylor, head of the National Community Reinvestment Coalition, said he, too, supports the idea of a national tracking system because it could force the industry to be accountable for mortgage paperwork. But he doubted whether MERS could fill this role.

“MERS was the personification of the darkest period of American finance, where Wall Street dictated to people in the real estate world the fact that they didn’t really care about underwriting standards anymore,” he said.

Lobbyists working for MERS include people who were prominent legislators or federal officials: former U.S. representative Bob Livingston and his former chief of staff, Allen Martin; John M. Duncan, assistant secretary of the Treasury for legislative affairs in the George W. Bush administration; and Arnold Havens, a former general counsel at Treasury. MERS is also under scrutiny by the Office of the Comptroller of the Currency, which oversees national banks. The OCC is taking the lead in an interagency examination of MERS and the accuracy of the information in its database. The agency is also sending personnel to look at the foreclosure process at large mortgage servicers and how they use MERS.

chaa@washpost.com dennisb@washpost.com

Lehman Brothers Holdings Inc., whose $11 billion suit against Barclays Plc is drawing to a close, is going after JPMorgan Chase & Co. as the next deep pocket to pay creditors in the biggest U.S. bankruptcy.

Lehman sued JPMorgan for $8.6 billion in collateral and tens of billions in damages, claiming the bank and Chairman James Dimon helped cause its collapse. The second-biggest U.S. bank twice asked a judge to dismiss the lawsuit. It said it was protected by a law governing the $467 trillion market for swaps and repurchase agreements when it lent Lehman’s failing brokerage $100 billion a day during the 2008 financial crisis.

JPMorgan’s defense hinges on so-called “safe harbor” laws, which allow clearing banks handling securities trades to take collateral from dealers without getting sued if a bankruptcy occurs later. Debtors can undo some transfers of assets done close to a bankruptcy filing. Banks invoke safe- harbor laws to oppose return of the money.

“Lehman has some viable claims here, so the real question is going to be the scope of the safe-harbor provisions,” said Stephen Lubben, a bankruptcy professor at Seton Hall University School of Law in Newark, New Jersey.

JPMorgan, based in New York, has argued in court papers that safe-harbor laws “present an insurmountable legal obstacle to Lehman’s lawsuit.” Losing that argument may hurt confidence in the market for swaps, repos and securities contracts, lawyers said.

A victory for Lehman would help its creditors, who the company has said stand to get an average of 15.8 cents on the dollar without any contribution from JPMorgan, which last month reported third-quarter net income of $4.42 billion.

‘Chain Reaction’

Without safe harbors, Lehman’s bankruptcy might have brought down other firms in a “chain reaction” as banks stopped lending to them, JPMorgan told U.S. Bankruptcy Judge James M. Peck in Manhattan in an Oct. 19 request to have the case dismissed. Lehman hasn’t filed a written response yet.

In Lehman’s favor is an attitude among bankruptcy judges that “all creditors should be equal in bankruptcy, but the safe harbor says some have advantages,” said Guy Dempsey, a lawyer in New York with Katten Muchin Rosenman LLP who specializes in derivatives and bank regulation.

Some judges think safe-harbor laws are clear, and they leave it alone, he said. “Others conclude the law is not clear so they need to interpret and modify it,” he said.

Peck, who handles Lehman’s bankruptcy, has at least twice ruled against Lehman creditors who asserted that their rights trump safe-harbor laws. Metavante Corp. and Swedbank AB appealed his rulings in a higher court. Metavante later decided to settle with Lehman; Swedbank’s appeal is ongoing.

2011 Trial

JPMorgan spokesman Joseph Evangelisti declined to comment, as did Peck, through his assistant Lynda Calderon. Peck may rule on the Barclays case in January or February and hold hearings on the suit against JPMorgan next year, said lawyers in the two cases.

Dimon promised former Lehman Chairman Richard Fuld he would return collateral a day before Lehman’s bankruptcy filing, and didn’t do so, Lehman said in a September filing. Earlier, it accused JPMorgan of using its “life and death power” as clearing bank to the brokerage “to siphon billions of dollars in critically needed assets.”

Lehman hasn’t proved Dimon promised anything, JPMorgan said in a filing.

Swaps trades, protected by safe harbor, total $467 trillion globally, the International Swaps and Derivatives Association, or ISDA, estimates. The figure doesn’t show how much money is at risk because many trades offset each other. Daily loans in the so-called tri-party repo market where JPMorgan lent money to Lehman were $2.8 trillion in 2008, according to the bank.

Split Argument

JPMorgan says all of its dealings with Lehman and its brokerage were governed by safe harbors. Peck might say the bank can’t be sued for taking collateral from Lehman’s brokerage to support its trades, and that it can be sued for taking assets from the Lehman holding company, Lubben said.

Arguably, taking collateral from the brokerage’s parent wasn’t directly related to repo trades, so it wasn’t protected by safe harbor, he said.

Lehman, once the fourth-largest investment bank with assets of $639 billion, foundered on Sept. 15, 2008, because of risky real estate bets and too much debt, including repos that it tried to hide from investors, according to bankruptcy examiner Anton Valukas’s report.

Lehman might have grounds to sue JPMorgan, he said. The suit is scheduled to be tried by Peck in 2012.

The bankruptcy case is In re Lehman Brothers Holdings Inc., 08-13555, U.S. Bankruptcy Court, Southern District of New York (Manhattan). The adversary case is Lehman Brothers Holdings Inc. v. JPMorgan Chase Bank NA, 10-03266, U.S. Bankruptcy Court, Southern District of New York (Manhattan).

To contact the reporter on this story: Linda Sandler in New York at lsandler@bloomberg.net.

To contact the editor responsible for this story: David Rovella at drovella@bloomberg.net

Nov 10

18

Chase will add jobs in Westerville

By BRET LIEBENDORFER

Published: Wednesday, November 17, 2010 3:21 PM EST

The current economic hardships are bringing more jobs to Westerville for the city’s largest employer, JPMorgan Chase.

The company plans to hire more than 100 new employees at its John G. McCoy Campus, a four-building office complex at 340-380 S. Cleveland Ave. in Westerville.

“It will be 120 additional mortgage specialists that will work in serving the default area including (loan) modifications, short sales and foreclosures,” said spokeswoman Mary Kay Bean.

Positions include quality specialists who review mortgage documents to ensure compliance with company procedures, senior operations specialists who process documents used in loan servicing, and quality control managers who monitor workflow quality and consistency.

All jobs require a high school education and previous loan experience. Interviews were held in an invitation-only job fair Tuesday, Nov. 16, open only to those who previously applied online with the company.

Bean said the company does not release salary details, but said they are competitive and include a compensation package consisting of medical coverage, a 401k, employee stock purchase plan and paid vacation.

Christa Dickey, Westerville community affairs coordinator, said the city did not work with the banking giant to bring the jobs to town and they are not part of the 150 the company announced in June 2009 as part of a plan to add 1,500 jobs in Central Ohio over three years.

Between the Cleveland Avenue campus and its credit card processing center at 800 Brooksedge Plaza, JPMorgan Chase already employs about 3,400 in Westerville.

By David Benoit

NEW YORK (MarketWatch) — J.P. Morgan Chase Co. Chief Financial Officer Doug Braunstein said Wednesday the bank remains working very hard with regulators and enforcement officials about the investigations into home foreclosures, and that he is hoping for a conclusion soon.

Braunstein, speaking at a conference, said he wouldn’t comment on discussions with the state attorneys general or regulators, but that the bank is toiling to reach the right conclusion.

He reiterated what other J.P. Morgan (JPM 39.84, +0.66, +1.67%) executives have said recently, that the foreclosure moratorium is costing the bank “a couple hundred of million” dollars each month it is in place, but that the bank is confident it hasn’t foreclosed on anyone who didn’t deserve foreclosure.

“Foreclosure is the last resort and we work very hard to avoid it,” Braunstein said at the Bank of America Merrill Lynch Banking and Financial Services Conference, adding J.P. Morgan has modified mortgages twice as much as it has foreclosed on homes.

The banking industry has now been in the midst of a foreclosure storm for the past few months, with claims that the processes they employed to handle the soaring number of foreclosures were improper. J.P. Morgan was among the big lenders who put a stop to all foreclosures as it reviewed its procedures. Braunstein didn’t comment on how much longer he expected the moratorium to continue, though another J.P. Morgan executive had said earlier this month it could end within a few weeks.

On the other major mortgage issue facing the banks, Braunstein reiterated J.P. Morgan’s position that it believes it is through the worst of the demands from government-sponsored enterprises that the banks repurchase the deals that made up mortgage-backed securities. He also argued that the private-investors who try to demand the repurchases, known as putbacks, face much higher hurdles than the government-sponsored enterprises.

Braunstein also touched on the credit market and the company’s still high loan-loss reserves. He said that delinquency and severity of losses the bank saw at the end of the third quarter have remained constant, an important note because he said again if loan losses are stable J.P. Morgan “may very well be forced to release some reserves.”

J.P. Morgan’s third-quarter profit was significantly boosted by the release of $1.7 billion from its loan-loss reserves.

said Wednesday the bank remains working very hard with regulators and enforcement officials about the investigations into home foreclosures, and that he is hoping for a conclusion soon.

Braunstein, speaking at a conference, said he wouldn’t comment on discussions with the state attorneys general or regulators, but that the bank is toiling to reach the right conclusion.

He reiterated what other J.P. Morgan executives have said recently, that the foreclosure moratorium is costing the bank “a couple hundred of million” dollars each month it is in place, but that the bank is confident it hasn’t foreclosed on anyone who didn’t deserve foreclosure.

“Foreclosure is the last resort and we work very hard to avoid it,” Braunstein said at the Bank of America Merrill Lynch Banking and Financial Services Conference, adding J.P. Morgan has modified mortgages twice as much as it has foreclosed on homes.

The banking industry has now been in the midst of a foreclosure storm for the past few months, with claims that the processes they employed to handle the soaring number of foreclosures were improper. J.P. Morgan was among the big lenders who put a stop to all foreclosures as it reviewed its procedures. Braunstein didn’t comment on how much longer he expected the moratorium to continue, though another J.P. Morgan executive had said earlier this month it could end within a few weeks.

On the other major mortgage issue facing the banks, Braunstein reiterated J.P. Morgan’s position that it believes it is through the worst of the demands from government-sponsored enterprises that the banks repurchase the deals that made up mortgage-backed securities. He also argued that the private-investors who try to demand the repurchases, known as putbacks, face much higher hurdles than the government-sponsored enterprises.

Braunstein also touched on the credit market and the company’s still high loan-loss reserves. He said that delinquency and severity of losses the bank saw at the end of the third quarter have remained constant, an important note because he said again if loan losses are stable J.P. Morgan “may very well be forced to release some reserves.”

J.P. Morgan’s third-quarter profit was significantly boosted by the release of $1.7 billion from its loan-loss reserves.